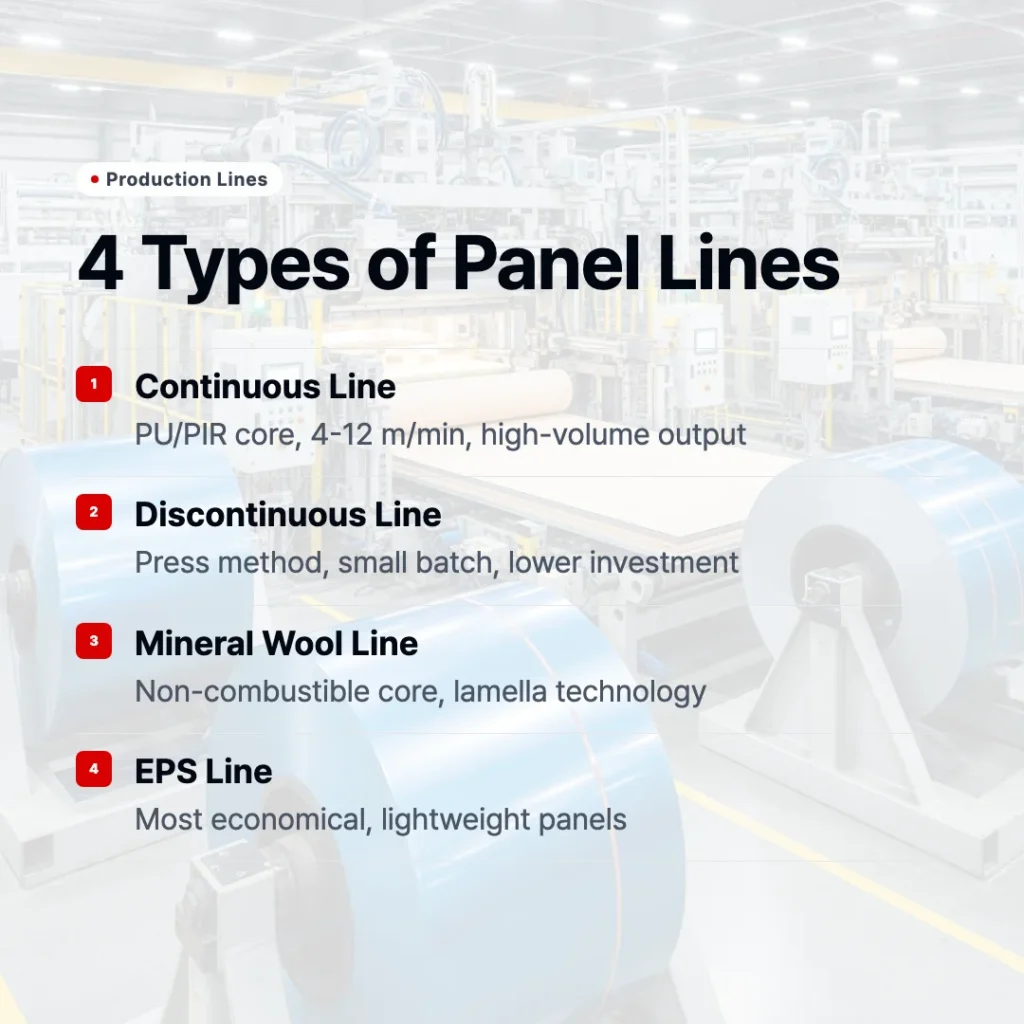

In this article, we will explore the key differences between mineral wool and polyurethane panel production lines — covering material handling, equipment configuration, capital investment, operating costs, and market positioning — to help manufacturers make an informed decision about which line type to invest in.

For any factory owner or investor evaluating entry into the sandwich panel manufacturing sector, or an existing producer considering capacity expansion, the choice between a mineral wool (MW) line and a polyurethane (PU) line is one of the most consequential decisions in the entire project. Both technologies produce insulated metal-faced sandwich panels, but behind the shared end product lies a fundamentally different set of raw materials, process logic, equipment architecture, and business economics. Getting this choice right from the outset determines not just profitability, but also which market segments you can serve and how your factory will operate day to day.

Core Material Handling Differences

The most visible difference between the two line types begins before production even starts — in how raw materials are received, stored, and prepared for processing.

On a mineral wool line, the primary input material arrives as compressed wool bales. These bales must be stored in a dry, covered warehouse — typically a dedicated area of 500 to 1,000 square meters depending on production volume — away from moisture and contaminants that could degrade fiber integrity. Before entering the production line, the wool bales are opened and fed into a lamellar cutting system. This is one of the most distinctive features of mineral wool production: the lamellar process slices the wool mat and re-orients the fibers perpendicular to the panel face, turning what would be horizontally layered fibers into a vertical configuration. This 90-degree re-orientation is critical because it dramatically improves the compressive strength and bonding surface area of the core, which in turn allows the adhesive to form a strong, durable bond with the metal facings.

Adhesive preparation is another dedicated process step that has no direct equivalent in PU production. A two-component adhesive system — typically a polyurethane-based or phenolic adhesive — must be mixed and maintained at the correct viscosity and temperature before application. Adhesive storage tanks, metering systems, and heated application rollers add to the equipment footprint and require regular maintenance to prevent clogging or inconsistent coverage.

On a PU line, the raw material handling environment looks entirely different. The inputs are liquid chemicals: polyol and isocyanate, stored in temperature-controlled holding tanks. These are the two reactive components that, when mixed under high pressure in a mixing head, undergo an exothermic chemical reaction and expand into the rigid foam that forms the panel core. Because isocyanate is a hazardous chemical — requiring proper ventilation, personal protective equipment, and strict handling protocols under regulations such as REACH in Europe and equivalent frameworks in other regions — a PU facility must include a dedicated chemical storage area with spill containment, fume extraction systems, and emergency response provisions.

Temperature management for the liquid raw materials is non-negotiable. Polyol and isocyanate must both be held within a precise temperature window — typically 18 to 22 degrees Celsius — to ensure consistent reactivity and foam cell structure. Refrigerated storage or climate-controlled tank rooms are therefore standard features of any serious PU facility. In climates with significant seasonal temperature variation, this adds to operating costs year-round.

From a space planning perspective, a MW line generally requires more floor area for bale storage and lamellar handling equipment, while a PU line requires more investment in chemical containment infrastructure. Safety compliance costs are higher for PU due to the chemical nature of the inputs.

[Internal Link: sandwich panel line types → Sandwich Panel Production Line: Types, Technology & How to Choose]

Line Speed and Curing Process Comparison

The production throughput of a sandwich panel line is governed by how quickly the core material can be properly bonded to the facings — and this is where MW and PU lines diverge most significantly in terms of process logic.

On a mineral wool line, curing is driven by adhesive chemistry rather than a self-generating chemical reaction. After the adhesive is applied to the metal facings and the lamellar wool core is positioned between them, the assembled panel passes through a heated press or laminating conveyor. The adhesive must reach its activation temperature and sustain contact time sufficient for a complete bond to form. Depending on adhesive type, panel thickness, and press temperature, dwell time in the press zone typically ranges from 5 to 20 minutes for discontinuous (press-based) systems. Even on continuous MW lines — where a moving belt replaces a stationary press — the bond time constraint limits line speeds to approximately 3 to 6 meters per minute under most operating conditions.

The output capacity of a mineral wool line, measured in square meters per hour, is therefore substantially lower than that of a comparable PU line. A mid-range continuous MW line might produce 1,000 to 2,000 square meters per shift, whereas a comparable PU continuous line can output 2,500 to 5,000 square meters per shift at speeds of 6 to 12 meters per minute.

On a PU line, the foaming reaction itself generates heat — a property known as exothermic behavior. Once the polyol and isocyanate are mixed and injected between the facings, the foam begins to expand and cure almost immediately. The double-belt conveyor that transports the panel through the curing zone supplements this with external heat to accelerate and standardize the reaction, but the exothermic nature of the foam means curing proceeds rapidly — typically within 4 to 12 minutes total from injection to fully cured panel. This is why PU lines can run at significantly higher speeds.

However, the exothermic reaction also creates a management challenge: if heat build-up inside the panel is not properly controlled — particularly in thick panels of 150 mm or more — the foam can over-expand, cause delamination, or produce an uneven cell structure in the core center. Managing the balance between line speed, belt zone temperature, foam formulation, and panel thickness requires careful recipe development and real-time process monitoring.

KINDUS engineers production lines with PLC-controlled temperature management across both MW and PU configurations, enabling operators to maintain consistent product quality across thickness ranges and ambient conditions.

[Internal Link: PU/PIR machine overview → PU/PIR Sandwich Panel Machine: Complete Technical Overview]

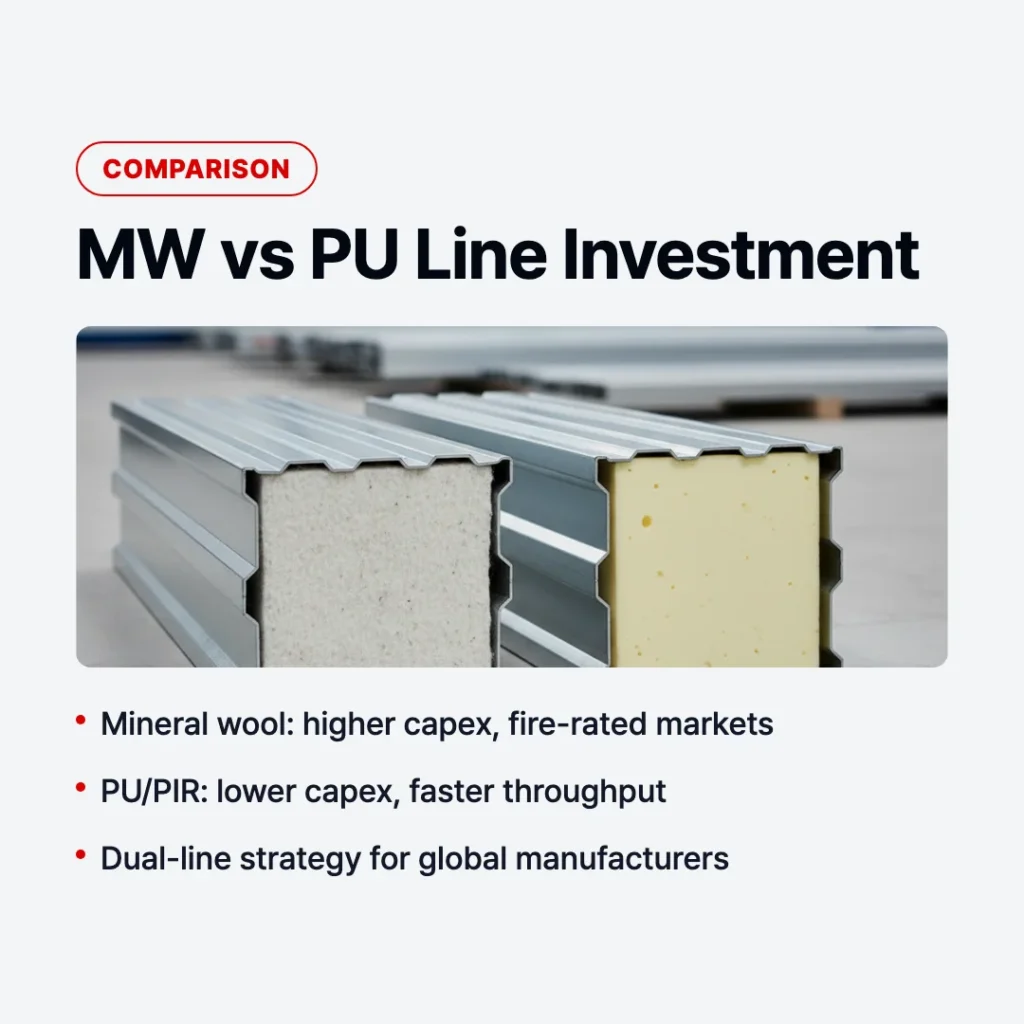

Equipment Investment and ROI Analysis

Capital expenditure is often the first factor operators evaluate when comparing line types, but the full picture requires examining both initial investment and ongoing operating economics.

In terms of capital expenditure, a PU continuous line and a MW continuous line of comparable panel width and output capacity sit in a broadly similar price range for the core machinery. However, the total project cost diverges when ancillary infrastructure is included. A PU line requires investment in a chemical storage room with containment and ventilation, high-pressure metering and mixing equipment (which carries a higher unit cost than MW adhesive systems), and often additional fire suppression provisions. A MW line requires investment in the lamellar cutting system, adhesive preparation and heating equipment, and a larger warehouse footprint for bale storage.

For a greenfield investment, the total installed cost of a PU line — including site preparation, chemical handling infrastructure, and commissioning — typically ranges from USD 1.5 million to USD 4 million for a mid-capacity continuous line. A MW line of equivalent output capacity generally falls in the USD 2 million to USD 5 million range, reflecting the more complex material handling and bonding process. These are indicative ranges; actual project costs depend on line speed, panel specification, degree of automation, and local civil construction requirements.

Operating cost differences are significant over the life of the equipment. Raw material costs per square meter of panel produced depend heavily on local market pricing for wool versus chemicals, but mineral wool typically carries a higher per-unit cost than PU foam at equivalent panel thickness. Energy consumption on a MW line is often lower than on a PU line because there is no need to maintain chemical tanks at precise temperatures year-round. Labor requirements tend to be higher on a MW line due to the more manual nature of bale handling and lamellar positioning, particularly on discontinuous lines.

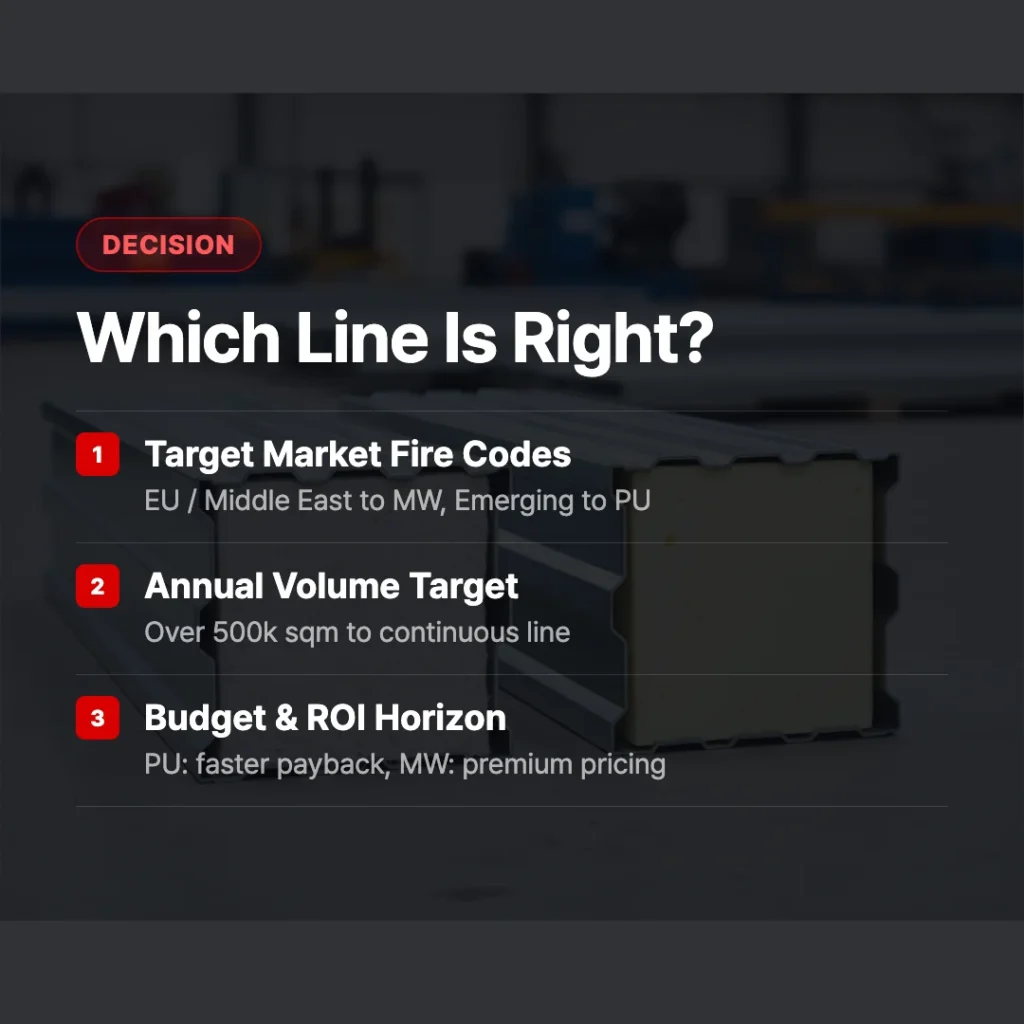

Payback period analysis should therefore be modeled against the specific panel type, target selling price, and local production cost structure. In markets where fire-rated MW panels command a premium of 20 to 40 percent over standard PU panels — as is common in Northern Europe and parts of the Middle East — the higher capital and operating costs of a MW line can be recovered within 3 to 5 years at moderate production volumes. In cost-driven markets where standard PU panels are the primary product, the lower operating cost and higher throughput of a PU line typically yields a faster payback.

What is the total investment cost difference between a mineral wool line and a PU line?

For comparable output capacity, the total installed cost of a MW line is typically 20 to 40 percent higher than a PU line when all infrastructure — including material handling, adhesive systems, and warehouse requirements — is included. However, the MW line produces a higher-value product in fire-regulated markets, which can offset the higher capex through better margins. A detailed ROI model specific to your target market and production volume is the most reliable basis for comparison.

Operator Skill Requirements

The human factor in production line operation is often underestimated during investment planning, but it has a direct impact on product quality, waste rates, and operational uptime.

A mineral wool line demands a higher degree of manual operator involvement, particularly in the material preparation stages. Workers handling bale opening, lamellar cutting setup, and adhesive application must understand how fiber orientation affects panel strength, how adhesive coverage uniformity relates to delamination risk, and how to adjust press settings for different panel thicknesses. While none of these skills require advanced academic qualifications, they do require hands-on training and a period of supervised operation before an operator can work independently. Training new operators on a MW line typically takes 4 to 8 weeks before consistent quality output is achieved.

Wool fiber handling also presents an occupational health dimension. Mineral wool fibers, if inhaled in significant quantities, are classified as a potential respiratory irritant. Operators must consistently use appropriate respiratory protection and work in areas with adequate ventilation. Establishing a disciplined safety culture around fiber handling is an ongoing management responsibility.

On a PU line, the emphasis shifts toward chemical safety competency and automated system management. Operators must understand the hazard profile of isocyanate — a sensitizer that can trigger occupational asthma — and adhere strictly to exposure controls including respiratory protection, glove use, and emergency spill response procedures. At the same time, the more highly automated nature of a PU continuous line means that day-to-day production monitoring is largely accomplished through the PLC/HMI interface, where operators adjust parameters and respond to alarms rather than physically handling material at each process step.

The key skill on a PU line is understanding the relationship between dosing ratios, line speed, curing temperature, and foam quality — and being able to diagnose and correct deviations before they result in off-specification panels. This requires operators who are analytically capable of interpreting process data and making systematic adjustments, rather than primarily relying on hands-on dexterity.

Staffing requirements differ accordingly. A mid-capacity MW line typically requires 6 to 10 operators per shift, while a comparable automated PU line can be run with 4 to 7 operators. Over the life of a factory, this difference in labor headcount translates into a meaningful operating cost gap that should be factored into any investment comparison.

Market Demand Trends by Region

Understanding where demand for each panel type is growing — and why — is as important as understanding the production differences when making a line investment decision.

In Western Europe, fire safety regulations are the dominant driver of panel type selection. Standards such as EN 13501-1 and national building codes in Germany, France, the United Kingdom, and Scandinavia mandate non-combustible or limited-combustibility core materials for a growing range of building applications including facades, roofing, and interior partitions in commercial and public buildings. Mineral wool panels — classified as Euroclass A1 or A2 non-combustible — meet these requirements by definition, while PU panels must be PIR formulated and tested to achieve comparable ratings. This regulatory environment has made MW panels the preferred specification in high-rise commercial construction and public infrastructure across much of Western Europe, creating sustained demand for MW panel production capacity.

In the Middle East, a combination of fire safety mandates and extreme climate conditions drives demand for high-performance panels. Countries including Saudi Arabia, the UAE, and Qatar have tightened building fire codes following a series of high-profile facade fires, and specifications increasingly require Class A non-combustible panels for commercial and residential towers. At the same time, the extreme heat of the region makes thermal performance critical, placing a premium on panels that deliver both fire safety and insulation efficiency. MW panels satisfy both requirements and command premium pricing in these markets.

In emerging markets across Sub-Saharan Africa and Southeast Asia, the calculus is different. Construction budgets are more constrained, fire codes are often less stringent or less consistently enforced, and the primary driver of panel selection is cost per square meter. PU panels — lower in production cost, faster to manufacture, and available from a larger base of regional suppliers — dominate these markets. The relatively lower capital investment required to establish a PU line also makes it more accessible to local entrepreneurs entering the panel manufacturing sector for the first time.

For manufacturers with the capital to invest in dual-line capability, operating both a MW line and a PU line provides access to the full spectrum of market demand. A factory that can produce both panel types is positioned to serve regulated markets with high-value MW products while supplying cost-sensitive markets with competitively priced PU panels — significantly broadening the addressable customer base and reducing exposure to single-market demand cycles.

KINDUS has supported clients in both line configurations, including dual-line factory setups, across projects in more than 40 countries. The company’s market knowledge, accumulated over 30 years and 170-plus delivered projects, provides a practical basis for helping clients match their line investment to the specific demand profile of their target markets.

Checklist: Key Factors for Deciding Between a Mineral Wool Line and a PU Line

- Does your primary target market have building fire codes that require Class A non-combustible panels? If yes, a MW line is necessary.

- Is your target selling price positioning in the premium (fire-rated) or standard (cost-efficient) segment?

- What is the realistic annual production volume in your plan, and does the throughput of each line type support it?

- Do you have access to a reliable local supply of mineral wool bales, or is isocyanate/polyol more readily available?

- What is the labor cost environment in your country, and how does the operator headcount difference affect your operating cost model?

- Do you have the infrastructure to safely handle and store hazardous chemical inputs (PU) or manage fiber handling and adhesive systems (MW)?

- Are you targeting a single market or planning to export to multiple regions with different regulatory environments?

- Is dual-line capability a viable option given your available capital and facility size?

Link for mineral wool line technology is Mineral Wool Sandwich Panel Production Line: Technology & Specifications]

Frequently Asked Questions

Which production line is more expensive — mineral wool or PU?

On a like-for-like output capacity basis, a mineral wool line generally carries a higher total installed cost than a PU line — typically 20 to 40 percent more when all material handling infrastructure, adhesive systems, and warehouse requirements are included. The MW line also tends to have higher per-unit raw material costs. However, the higher-value product it produces in fire-regulated markets often supports better margins, which can justify the additional investment. The right comparison is not just capital cost but full lifecycle economics including margins, throughput, and market pricing.

Can one production line produce both mineral wool and PU panels?

No — MW and PU panels require fundamentally different equipment architectures. A MW line uses dry fiber handling, lamellar cutting, and adhesive bonding, while a PU line uses liquid chemical storage, high-pressure mixing, and foam-based exothermic curing. These are not interchangeable processes. Manufacturers who want to produce both panel types need two separate lines. Some common equipment — such as roll forming units for facing preparation or stacking systems — may potentially be shared with customization, but the core production machinery is dedicated to each process.

Which panel type has higher market demand globally?

By volume, PU/PIR panels currently account for the larger share of global sandwich panel production, driven by their cost efficiency and widespread use in cold storage, industrial buildings, and emerging market construction. However, the fastest-growing segment by value is fire-rated panels — including both PIR and mineral wool — driven by tightening fire safety regulations in Europe, the Middle East, and increasingly in Asia. For a factory targeting long-term growth and premium market positioning, MW capability is becoming an increasingly important asset.